What you should know before investing

1. Know yourself

We all have different investing goals and different time frames for achieving them. Some are short-term, like saving for a vacation or a car, while others are long-term, like retirement. In addition, every investor has a different comfort level with investment risk.

While risk sounds like something to avoid, there can be an upside – the greater risk may offer the opportunity for greater rewards over the long term. Finding a balance between risk and reward that you’re comfortable with – and that’s appropriate for your investment time frame – is an important first step to successful investing.

To better understand yourself as an investor, consider your: risk tolerance, investment knowledge, investment objectives, gross annual income, approximate net worth, and investment time horizons.

2. Get an early start

Taking advantage of the effects of “compounding” is one of the best ways to make your money work for you. Compounding is money multiplying itself by earning a return on the return.

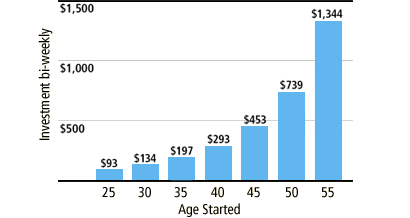

Starting early makes it easier

This chart demonstrates the bi-weekly investment needed to reach $500,000 by the age of 65. (For example, if you started investing at 25 years old, you would need to contribute $93 every two weeks.)

What is “asset allocation”?

The mix of investments within your portfolio is also known as your portfolio’s asset allocation. A diversified portfolio typically holds a combination of savings income and growth investments.

3. Invest regularly

It’s generally much easier to come up with a smaller amount to invest on a monthly or weekly basis than to make a large, lump-sum contribution. A regular investment plan allows you to choose when and how often you make contributions – ensuring you make investing a priority. With a CIBC Regular Investment Plan, money will be automatically withdrawn from your account and invested in a range of CIBC investment solutions. You can invest with pre-authorized contributions of as little as $25 a month.

How can I lower the average cost of investing?

Investing smaller amounts in mutual funds over time – or “dollar-cost averaging” – can mean lower average costs than if you make infrequent purchases. For example, your money will buy more units of a mutual fund when prices are low; and fewer units when prices are high. Provided the fund gains in value over the long term, you’ll profit from your purchases during short-term price declines.

4. Build a diversified portfolio

Spreading your assets across a wide range of investments is an effective way to reduce risk and increase potential returns over the long term. Holding a mixture of different types of investments will help cushion your portfolio from downturns, as the value of some investments may go up while the value of others may go down.

5. Monitor your portfolio

You should examine your investment portfolio with a CIBC advisor, or on your own, at least once a year to ensure that it continues to meet your needs. Market conditions, life events (marriage, children, and retirement), and changing goals are cues to review your portfolio.

6. Align your investments with your time horizons

The type of investments you choose will depend on whether you’re saving for long-term or short-term goals. For your long-term goals, you may want to consider long-term, growth-oriented investments. Your short-term goals call for investments that are more conservative, and more accessible. For example, if you’re investing to save for a downpayment on a home, you’ll want quick and easy access to your funds.

| Short-term goals | Long-term goals | |

|---|---|---|

| What are they? | These are objectives that are less than 5 years away, for which you’ll need a significant amount of money. For example:

|

These are objectives that are 5 or more years away. For example:

|

| What to invest in: | To save for the short term, consider investments that are more conservative in nature and more easily accessible. | To save for the long term, you should consider a diversified portfolio that may include a growth component. |